We want to save employers the pain and expense of making late superannuation contributions for employees, or not paying them at all. Recent changes to the way the ATO apply penalties when superannuation contributions are paid late (even if only by a day) result in significant additional expense for employers.

The implementation of Single Touch Payroll (STP) means the ATO can easily identify employers that do not meet their strict superannuation guarantee obligations thereby ensuring non-compliant employers now rarely escape penalty.

When must superannuation contributions be paid?

Superannuation contributions must be received by the superannuation fund within 28 days of the end of a quarter. There is a common misconception that superannuation contributions must be paid by the employer by the 28th day after the end of the quarter. This is not correct. It is the date of receipt by the superannuation fund that is important. However, if you are using the ATO Small Business Clearing House and if the contributions are received by that clearing house by the 28th day following the end of the quarter, you will be treated as having made the contributions to the superannuation fund on time.

Why it is a bad deal to pay late or not at all

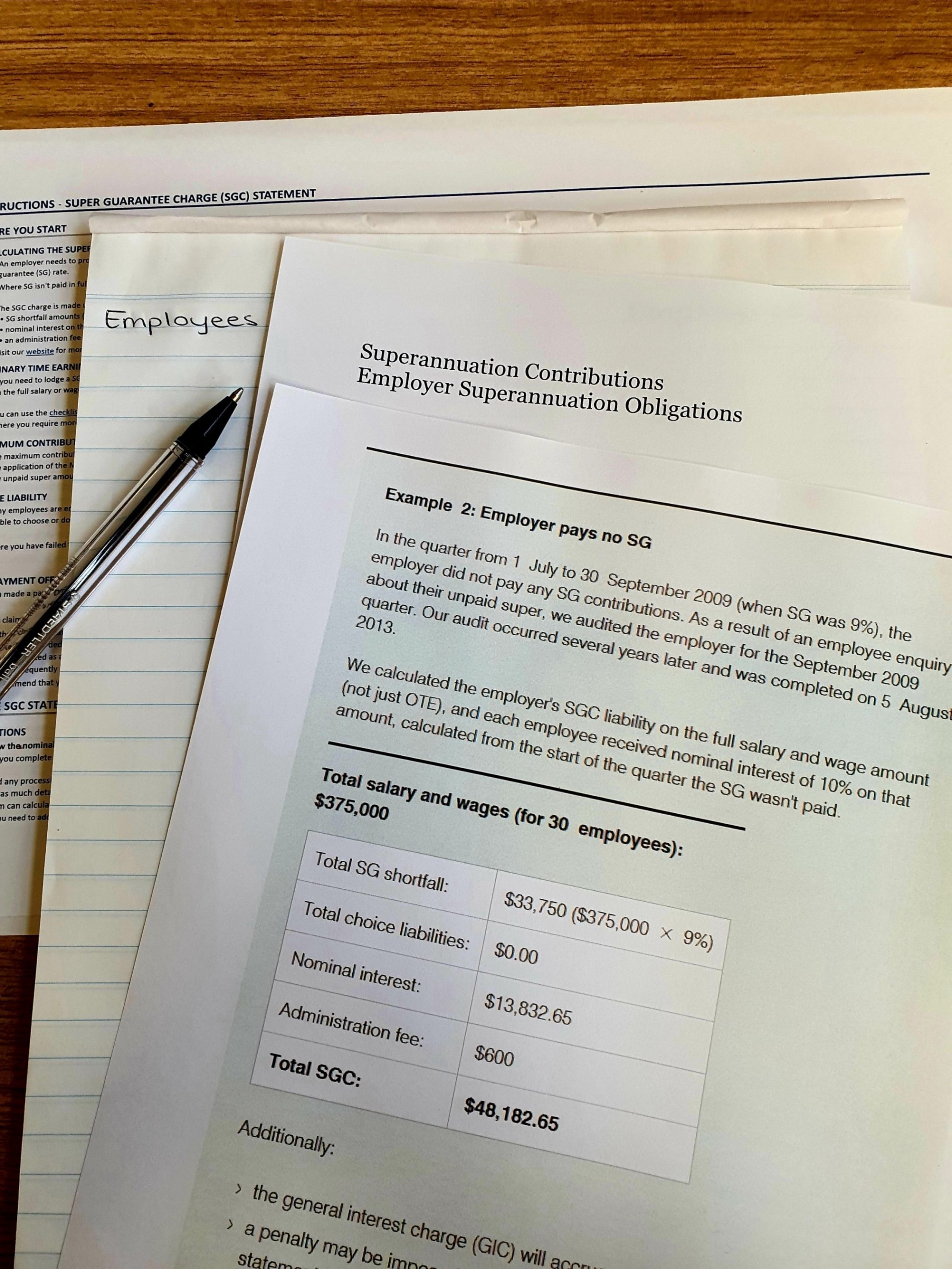

The Australian Superannuation Guarantee system is designed to penalise employers severely who pay superannuation contributions late or who do not pay the contributions. This is because the employer must pay, at least, the Superannuation Guarantee Charge (“SGC”). For a quarter this is:

- The late superannuation contributions; plus

- Extra contributions due to a higher earnings base being used; plus

- 10% interest calculated from the beginning of the quarter to the time of lodgment of the Superannuation Guarantee Statement or assessment; plus

- A $20 charge per employee.

In addition to the SGC, penalties can be levied if you have not lodged with the ATO a Superannuation Guarantee Statement. These penalties can be up to 200% of the SGC. Both the SGC and the penalties are not tax deductible. It will often be the case that the combined after-tax amount of the SGC and penalties is many multiples of the superannuation contributions paid late.

If an employee’s superannuation fund receives their superannuation contribution late (even if only by a day), the employer is required to complete and lodge a Superannuation Guarantee Statement to calculate the above-mentioned penalties payable. The sooner this is done, the lesser the penalty (given the 10% interest levied).

We encourage you to watch this short video give to you more information about this issue. Please contact our office should you have any queries.